Life Insurance

Last 10 years has witnessed a growing awareness in this space, over 26 multinational companies have set their joint venture in India and have been competing with the local insurer Life Insurance Corporation of India. This competition has mainly resulted in popularising 2 category of product to which Indian customers were naive.

Unit Linked Insurance Plan

Pure Term Insurance Plan

Online Term Plan

Recently some of the Insurance Brokers have started to market the Pure Term Insurance Plan also know as Term Assurance plans very aggressively and have resorted to TV advertisements leading to huge media spend thereby increasing the Cost of Sales. These Insurance Brokers play the role of Marketers offering comparison advantage across product to the Customer. However the comparison offered by them is solely emphasizing on Price while ignoring the other important features of the product offered by the insurer. Undoubtedly price play an important role to achieve competitive advantage nevertheless other feature cannot be ignored e.g. Bajaj Allianz Life Insurance offers joint life Term Assurance Plan offered by none in the Industry and they offer discount on joint life ranging from 1% to 5% on the premium which makes their product more competitive than buying 2 individual products by a couple. The marketing portals offering comparison completely ignores this factor of Joint Life as their software is designed only for Single Life.

Hence customers are

advised to not to solely rely on these Comparative websites

offering only price advantage while completely ignoring other

product features which are of more importance in decision making.

As customer we do not buy insurance very often hence a plan

offering comprehensive solution to our needs are of more

importance.

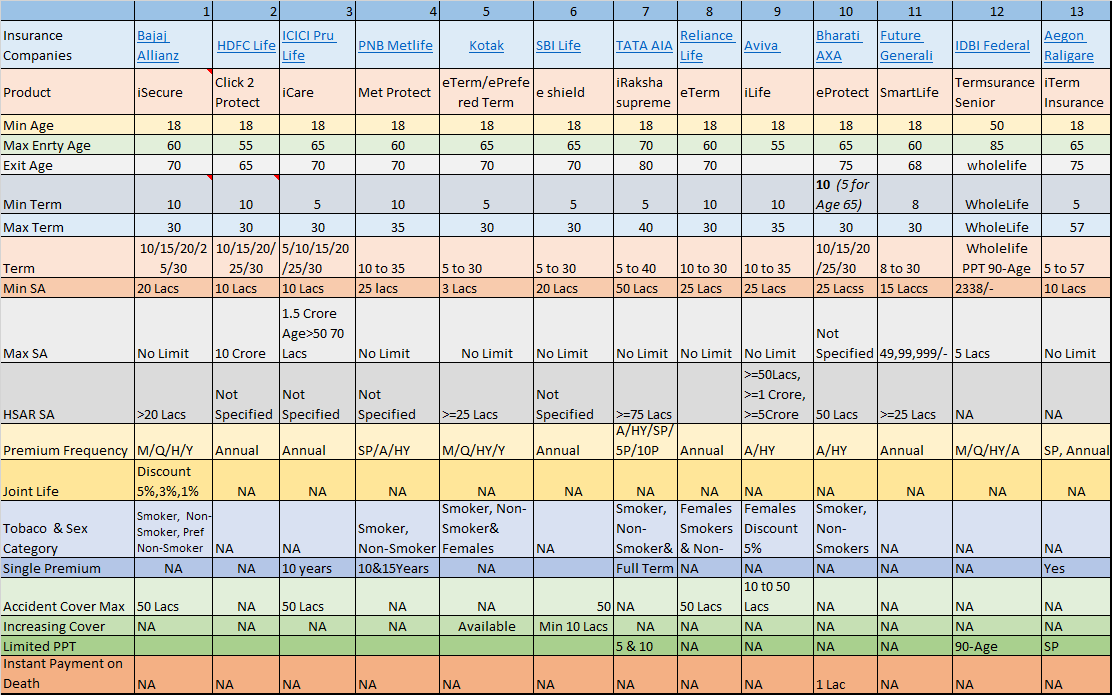

The below chart provides a comparison of all the Term Assurance/ Pure Insurance products in the Life Insurance Industry across all the parameters which will aid a prospective buyer to take the right decision as per his need and requirements.

Once you have shortlisted a few products from the below list, I will suggest the next step to proceed further in your buying process of a Term Assurance Plan. If you don't have time to read the chart just skip the chart and go to the next section of the page.

Legends PPT: Premium Paying Term, HSRA : High Sum Assured Rebate, NA Not Applicable/ Not Available,

M/Q/H/Y/A : Monthly/Quarterly/Half Yearly/Yearly/Annual, SP: Single Premium.

The Thumb rule one should bear in mind while selecting a pure Term assurance plan is that select the plan which will cover you for maximum Number of years for e.g. in the above chart Maximum Term Offered by most of the companies are for 30 years, hence a person aged 30 is opting for such plan will not be insured after his age 60, the company stands to gain substantially in such situation as The probability of a person dying before 60 is far less then he dying after 60. Moreover after 60 very few companies insure a person and even if they do the same comes at a very high cost, the probability of a person's insurability due to ill health also diminishes drastically. One does not buy insurance that often hence proper care needs to be taken whenever you buy the same it should be perpetual in nature.

Let’s Work out a few examples

Example 1.

From the above chart for a person aged 30 and below, I would suggest him to buy Aegon Raligare which will cover him till age 75 years, IDBI Federal which cover for whole of Life and TATA AIA covers him up till his age 80 years also seems attractive but there is a catch, The Entry age for IDBI Federal is 50 years and a person aged 30 years or below is not eligible for the same similarly in case of TATA AIA The maximum term is 40 years which will cover him till age of 70 years or less, hence i will not suggest to go for it.

In the above case any person aged 30 years or below should opt for Aegon Raligare without any second thought as the maximum term is 57 years with exit age of 75 years. The same is applicable for Persons from Age 31 to 34.

Example 2.

For a person aged 35 years the above chart features wise suggest between 2 products i.e. Aegon Raligare and TATA AIA as the coverage term for this age is same that is 40 years up till the age of 75 years. However you may use the services provided by Web Aggregators (Covered in later part of this page) to compare between these two, the resultant effect for age 35 years is that Aegon Religare is cheaper between the two and hence I would suggest you to go for Aegon Religare.

Example 3.

For persons aged from 36 to 49 years, I am suggesting to go for TATA AIA as they will be covered till the age of 76 to 80 respectively, which no other company offers. In this Age bracket of 36 To 49 years TATA AIA is a clear winner.

Example 4.

For persons aged between 50 to 85 years, from the above chart IDBI Federal is a clear winner as they insure for whole of Life in which case Death Claim is Guaranteed and you are sure to get the Amount of Life Cover, in which case the premium you are paying will not be wasted, this will be a prudent investment decision however there is a catch, the premium amounts for the higher age in this bracket are expensive which may make the buying decision prohibitive and hence it is suggested for persons between age 50 to 70 to compare the premium/price with the nearest competitor TATA AIA by making use of services provided by Web Aggregators ( Covered in detail in later part of this page) and then decide accordingly.

By now you would had gathered how simple it is to choose a Pure Term Life Assurance Plan, which was otherwise made out to be a very complicated subject. I am reminded of a scene in the popular movie 3 idiots which I would like to reproduce herebelow (On a lighter note).

As there are 26 players in the Life Insurance space each claiming their Pure Term Insurance plans to be the best and the cheapest, this has put the prospective buyer in a state of confusion in making a buy decision, some brokers have taken advantage of this situation and are publicizing the need for Comparing the products and then Buy.

In reality there is very little to compare, the choice is between only 3 players i.e. Aegon Religare, Tata AIA and IDBI Federal.

Depending on your Age choose one of the above example in which you are fitting into and go ahead with the plan. You don't need the use of expensive system using software and Meta search engines to select a plan. The brokers are only complicating the situation by over use of technology similar to the Astronauts speeding huge amount on inventing a Pen when a pencil could do the job for you.

Use the above chart select the policy plan which suits you and go to the respective company’s website and buy the plan. Alternately click the logo of the selected company available on the right column and buy the plan.

The Online Comparitive Websites i.e. the likes of Policybazaar.com use the most common and popular mode of marketing i.e. TV media Ads, they indulge in media hammering to attract the customers to their site. Their websites first capture the personal data of the customer and also data like age, term of policy etc which is required for calculating the premium, there after the website is redirected to another website of a Web Aggregator who calculates the premium and throws the result of the most competitive insurers, once the customer decides to Buy the products the website once again redirects to the company's Website from whom the customer has choosen. In short one buying process involves redirection and export of data to 3 websites involving 3 different organisation thus making the process expensive.

Web Aggregators are a new breed of professional organisations in the Insurance Industry who are appointed by the IRDA ( Insurance Regulatory & Development Authority) to provide unbaised comparison service via internet to the prospective buyers in arriving at an informed decision. Web aggregators cannot advertise for any company nor can promote any specific company or companies. They make use of comparetive software and helps the customer to find out who is the most competitive price.

The service provided by Web Aggregators is faced with limitation of comparison of products on price and overlooks the features of the products.

Invariably due to the features offered by the Comparitive Websites the prospective buyer ends up buying a product which may not be the most suitable product for him. This reminds me of a book " Why people buy things they don't need " by Pamela N. Dangizer.

|

List of Web Aggregators Approved by IRDA |

|||

| S.No | Name of the Applicant | Web Address | Period of Approval |

| 1 | iGear Financial Services Pvt. Ltd. | www.MyInsuranceClub.com | 10.07.2012 to 09.07.2015 |

| 2 | Accurex Marketing and Consulting Pvt. Ltd. | www.accuratequotes.in | 31.07.2012 to 30.07.2015 |

| 3 | Great Indian Marketing & Consulting Services Pvt. Ltd. |

www.insuringindia.com | 28.09.2012 to 27.09.2015 |

| 4 | Voila Consultancy Services India Private Limited |

www.buysmartpolicy.com | 23.11.2012 to 22.11.2015 |

| 5 | eMudhra Consumer Services Ltd. | www.emudhrainsurance.com | 23.11.2012 to 22.11.2015 |

| 6 | I Call Soft (P) Ltd. | www.sastapolicy.com | 07.12.2012 to 06.12.2015 |

| 7 | Policy Mantra Insutrade Pvt. Ltd. | www.policymantra.com | 07.12.2012 to 06.12.2015 |

| Disclaimer:- IRDA shall not be responsible for any act of misconduct/mis-selling by any entity other than the entities mentioned above. | |||