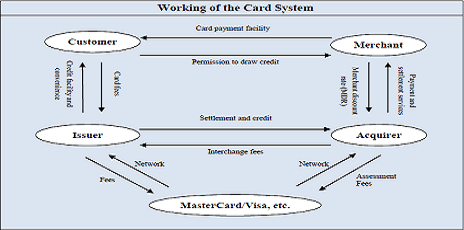

The system consists of a customer who holds a credit card from his issuing bank (called issuer), a merchant who has been given the facility of accepting credit cards by his acquiring bank (also called acquirer) and MasterCard/VISA, etc., whose networks are being used. In this system, first a merchant who decides to accept credit or debit cards in exchange for goods or services establishes a merchant account by forming a relationship with an acquiring bank. This relationship enables the merchant to receive sale proceeds from credit card purchases through credits in his account. However, while receiving such credits, the acquirer applies a Merchant Discount Rate (MDR), which is paid by the merchant to the acquirer in consideration for card acceptance services. A MDR is the percentage of sales that a merchant pays to the acquiring bank to process credit card transactions.

This rate generally varies from 1% to 3%. On the other hand, the cardholder pays charges in form of annual fee, finance charges, late payment charges, etc. to his card issuing bank. The risk of default by credit cardholders is borne by the issuing bank.

The Interchange fee on a purchase transaction flows from the merchant acquiring bank to the card issuing bank. The figure below explains the working of the Card System in India.

The settlement and credit transactions between the issuer

and the acquirer are done using the network of

MasterCard/VISA, who gets a share of the fee in exchange. In India,

though competition guides acquirer-merchant pricing policies, it is

generally understood that Interchange fees is one component of the

MDR established by acquirers. The implementation of proper

Interchange rates is necessary and also very crucial for

maintaining a strong and vibrant credit card payments network. The

other major component of the MDR is the fee imposed by the acquirer

which is retained by the acquirer to meet its own expenses. It is

quite common to see a transaction at a merchant establishment

involving a bank which is both the acquirer and the issuer. In such

a situation it may be possible to reduce the Interchange fee since

the payment network is substantially reduced. However, such reduced

Interchange fee is not generally passed on to the

merchants.

The settlement and credit transactions between the issuer

and the acquirer are done using the network of

MasterCard/VISA, who gets a share of the fee in exchange. In India,

though competition guides acquirer-merchant pricing policies, it is

generally understood that Interchange fees is one component of the

MDR established by acquirers. The implementation of proper

Interchange rates is necessary and also very crucial for

maintaining a strong and vibrant credit card payments network. The

other major component of the MDR is the fee imposed by the acquirer

which is retained by the acquirer to meet its own expenses. It is

quite common to see a transaction at a merchant establishment

involving a bank which is both the acquirer and the issuer. In such

a situation it may be possible to reduce the Interchange fee since

the payment network is substantially reduced. However, such reduced

Interchange fee is not generally passed on to the

merchants.

The banks and

MasterCard/VISA generate revenue and make profit in the credit card

system by charging Interchange fees. In the western countries big

merchants have already realized this and are in union in their

demand for reduction in Interchange fees. MasterCard USA,

moving towards being more transparent, has now explicitly

placed on it official web site the Interchange

Rates.

Source: Brief extract of paper publiished by Shri Ashish Das, Dept Of Mathematics IIT Mumbai, 10 Nov 2008